Jasmine Birtles

Your money-making expert. Financial journalist, TV and radio personality.

![]() Vicky Parry

5th Jan 2026

Vicky Parry

5th Jan 2026

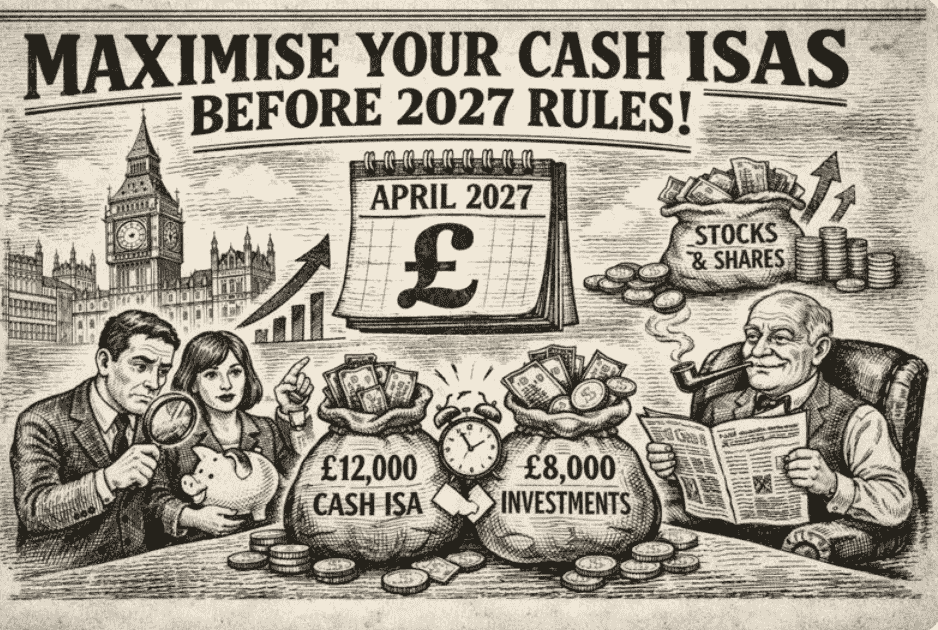

If you’ve been happily stashing money in your Cash ISA, there’s a big shake-up coming. From April 2027, under‑65s will see the annual allowance drop from £20,000 to just £12,000. Here’s how to make the most of your savings while you still can.

For many of us, Cash ISAs are the ultimate “set-and-forget” savings tool. They’re considered safe, straightforward, and, best of all, tax-free. But the next Budget has thrown a curveball. Suddenly, some of us will need to rethink how much we can put away each year — and where. The good news? With a bit of planning now, you can make the rules work in your favour.

The Government has announced that from 6 April 2027, anyone under 65 will only be able to put £12,000 a year into a Cash ISA. The overall ISA allowance remains £20,000, but the remaining £8,000 must go into a Stocks & Shares ISA, Innovative Finance ISA, or other qualifying ISA type.

If you’re 65 or older, you can still enjoy the full £20,000 tax-free in a Cash ISA — lucky you. But for the rest of us, this is a wake-up call.

Essentially, the change means that Cash ISAs will no longer be enough to take full advantage of your annual ISA allowance. You’ll need to start thinking about other options — even if the idea of investing gives you the jitters.

Here’s the silver lining: the change doesn’t come into effect for another two tax years. You still have a window to take full advantage of the current £20,000 allowance.

Remember, ISA allowances don’t roll over. If you leave your allowance untouched, you lose it forever.

Pro tip: If you’ve been saving sporadically, now’s the time to front-load your contributions. Every pound you lock in now is safe from tax and safe from future rules.

Not all Cash ISAs are created equal. Some come with a “flexible” feature, which is basically a lifesaver if your cash flow isn’t entirely predictable.

A flexible ISA lets you:

Think of it like having a backup plan built into your savings. Just make sure your provider actually offers flexibility — it’s not universal.

From April 2027, your full £20,000 allowance will need to be split. This is where things get slightly trickier for cautious savers:

Even if the idea of investing makes you nervous, putting some money into a Stocks & Shares ISA doesn’t have to be scary. Think of it as diversifying your savings rather than taking wild risks. Over time, it could even outperform cash, especially as interest rates remain relatively low.

Cash ISAs aren’t your only tax-free option. If you’re juggling multiple financial goals — like saving for a home or a child’s education — other accounts can take some pressure off your main ISA:

Using these options strategically means you can grow your money tax-free without maxing out your adult Cash ISA too quickly.

One of the biggest mistakes savers make is letting cash sit in a regular savings account once they’ve used up their ISA allowance.

Interest earned outside an ISA is taxable after your personal savings allowance. That could mean paying 20% or more on interest you could have kept tax-free. Using your ISA space now protects your money from tax and ensures your savings actually grow.

Before 5 April 2026:

Between April 2026 & April 2027:

Future Planning:

The 2027 Cash ISA cut may seem like a blow, but with a little planning, you can stay ahead of the curve. By using your allowances now, exploring flexible accounts, and branching into other ISA types, you can continue to grow your savings tax-free.

Think of it as a chance to be smarter with your money — and to make every pound work a little harder before the rules change

The content of this article is for informational purposes only and should not be considered financial, investment, or legal advice. Readers should conduct their own research and seek guidance from a qualified financial adviser on any investment decisions.

Your money-making expert. Financial journalist, TV and radio personality.