Jasmine Birtles

Your money-making expert. Financial journalist, TV and radio personality.

![]() Marc Crosby

6th Jul 2015

Marc Crosby

6th Jul 2015

Guest article from StepChange

From flash games to fad diets, Facebook has a way of ‘knowing’ what kind of content is likely to catch your eye.

Let’s face it, debt and money problems are things that most people can find pretty relevant to their lives. With this in mind, it’s little surprise that some very interesting ads have been popping up lately.

These ads may talk about how the “banks no longer have the upper hand”, or tell you that there’s an oh-so-simple way for you to ditch your debts.

We at StepChange Debt Charity feel these are pretty bold statements to make, considering that the companies putting these ads out don’t know anything about you or your financial situation.

In order to ensure you’re treated fairly at all times, the Financial Conduct Authority (FCA) has imposed strict criteria on the kind of statements companies can make about the services they offer. All financial organisations must behave in a way that’s clear and not misleading, yet these ads don’t seem to be playing by the rules.

Let’s take a closer look at the way these ads are worded and why you need to be vigilant…

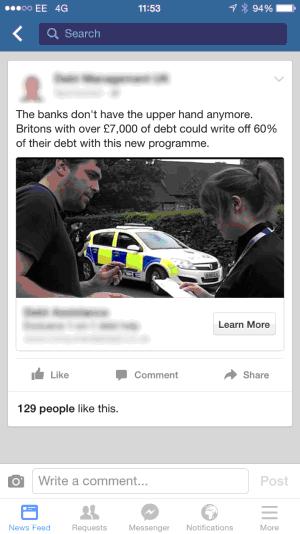

Does this look familiar?

What they’re saying: Britons with over £###### of debt can have ##% written off by paying £######.

Why it’s wrong: The only way to understand a person’s financial situation is by looking at their budget. Without understanding what you actually pay out and what comes in, how do they know what kind of debt solution is right for you?

What they’re saying: New Government legislation can help you write off ##% of your debt.

Why it’s wrong: Firstly the legislation they claim is ‘new’ isn’t actually new at all. Writing off a percentage of debt normally means putting a formal debt solution in place such as an individual voluntary arrangement (IVA) or bankruptcy.

These sorts of debt solutions have been around for a while. They’re certainly not to be considered an ‘easy way out’ and it’s very unwise to offer them without first understanding your situation. Understanding the risks of these solutions is just as important as understanding the benefits!

When the FCA outlined potential issues in the debt management market, one thing they found worrying was that people can sometimes make “quick, ‘distress’ purchases – (which) makes them more vulnerable to unfair or improper business practices.”

Simply put, this means that debt management companies shouldn’t make grand promises like this without knowing what you as an individual are dealing with. When you’re worried, you might make impulse decisions in order to make whatever’s troubling you go away. This includes handing over money to some firm who barely knows anything about you.

We speak to many people who are curious about this whole ‘wiping out your debts’ thing, but the truth is it’s very rarely that simple. If an ad like this makes a promise that seems too good to be true, then there’s a good chance it is.

For more information on the ‘debts written off’ myth, read this blogpost on MoneyAware. In the meantime, if you’re struggling with debts, our online advice tool Debt Remedy can help you put together a personal action plan in around 20 minutes. You can also speak to one of our friendly advisors about what you’re dealing with – visit our contact us page on our website to find out more.

Your money-making expert. Financial journalist, TV and radio personality.

Not so recently I went through a bankruptcy. I got bullied left, right and centre. Not so long ago I got contacted by someone who thought my ‘debt” was not paid off – when will it ever end?