Jasmine Birtles

Your money-making expert. Financial journalist, TV and radio personality.

![]() 156750

10th Feb 2020

156750

10th Feb 2020

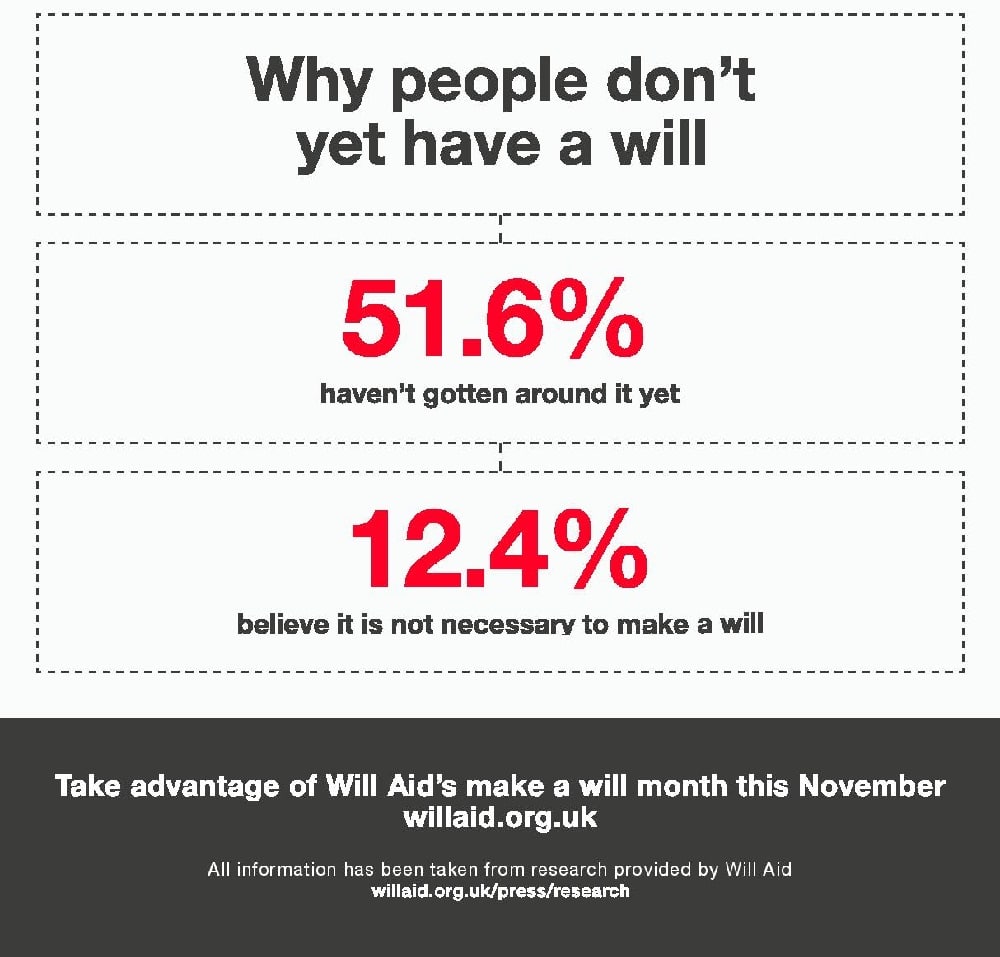

Find out how to get a will written with our easy guide. Ensure you don’t overpay in taxes or that your ex doesn’t end up with all your cash! Around two-thirds of us don’t have a will, which means cost and heartache to family and friends. So get it done now and you’ll feel a real weight off your shoulders! Read on for a handy and simple guide:

NOW!

No, really, whatever age you are, if you have any possessions, and certainly if you have any dependents, you should write a will.

It’s especially important for taking care of young children or other people who depend on you.

And even if you don’t, it’s about beating the tax man and having the last laugh!

If you’d like to give to charity when getting a will written, you could wait until November, which is Will Aid month. This is when solicitors and other will writers invite their customers to donate their fee to charity, so you can do good and get your will written in one go!

If you don’t make a will, then the law of intestacy applies.

If you don’t make a will, then the law of intestacy applies.

Broadly speaking, the law of intestacy reflects the common law of descent. This means that property usually goes first to a spouse, then to children and their descendants.

If there are no descendants, property will generally go to the parents of the deceased instead, then the siblings, the siblings’ descendants and so on to less immediate family members.

And if a person dies intestate with no identifiable heirs, the person’s estate tends to end up with the government. Do you want that? I doubt it!

There isn’t a government regulator for will writers. Technically anybody can write a will – without any qualifications – and providing it’s accurate and within the guidelines of the law, it will pass at probate.

However, because there’s no regulation, you need to be wary. As always, it’s best to use someone who subscribes to an accredited body. Members of The Society of Will Writers (SWW) and the Institute of Professional Will Writers (IPW) adhere to certain ethics and standards. Should you decide to write a will, it’s a good idea to make sure the company you want to use is certified by one of them. All SWW and IPW members are fully indemnified, trained, and supported in the laws of succession and estate planning.

Inheritance Tax (IHT) is a tax on death. The Government calls this tax a ‘voluntary tax’ which basically means that most of the time, with the right planning, you can avoid it.

IHT can reduce a beneficiary’s inheritance by a huge amount. At present, the IHT rate is 40% on any inheritance over £325,000. The £325,000 limit per person is called the ‘nil-rate band’.

For example, Tom leaves his son Harry £400,000 in his will. Tom is allowed to give £325,000 to Harry tax-free, but the £75,000 that exceeds the nil-rate band is taxed 40%.

40% of £75,000 is £30,000. Take this away from the full amount given to Harry and he is left with £370,000 inheritance – rather than the £400,000 his father left him.

Between married couples and civil partners, no inheritance tax needs to be paid. And under new laws, you can transfer any amount of the nil-rate band not used when one spouse (civil partner) passes away to the remaining spouse. So, a married couple can – in theory – leave a total of £650,000 to their children nil-rate.

The nil-rate band is transferred by percentage. Any percentage not used by the deceased is added on to the survivor’s nil-rate band.

For example, if a husband dies and leaves his entire estate (worth £350,000) to his wife, there is no inheritance tax to be paid.

The wife now has the £350,000 given to her by her husband, and a further £350,000 of her own money – meaning she has £700,000 to give away.

£650,000 of this is available to give away as a tax-free inheritance (her £325,000 nil-rate band, plus her deceased husband’s unused nil-rate band). But – the remaining £50,000 is still taxable.

With the law allowing married or civil partnership couples (not cohabiting couples) to transfer their nil-rate band, IHT planning is much simpler. Those who are married and with a combined estate is worth less than £650,000 don’t have to plan ahead for it.

If you’re married or living with a civil partner – and your personal estate is worth less than £325,000 – you also have nothing to worry about (although it’s essential you make a will if you want to leave your estate to your partner and you’re not married).

If you’re single or your combined estate exceeds the nil-rate band (currently £325,000 each), it’s important that you get professional advice to avoid IHT – ideally from a good tax accountant and/or lawyer. Independent Financial Advisers should be able to help too. Here are some options you might like to consider:

Gifts over £3,000 per year given less than 7 years before you die will incur some IHT, as will any gifts exceeding the total £325,000 allowance. This tapers off towards the 7-year mark: anything less than 3 years is taxed at 40%, tapering down to 8% tax on 6 years.

You could also consider a discretionary trust to avoid IHT.

Essentially, a discretionary trust is a way of cutting down the tax your family and friends would have to pay if they were simply left all of the money in your will. The downside for them is that other people, trustees that you have appointed, pay money to the beneficiaries at their own discretion according to the rules you’ve laid down.

For example, a man leaves £250,000 in a discretionary trust, with his wife as a trustee and his two children as beneficiaries. The wife has full control over the money in the trust, and when it’s paid out the children have no right to demand the money.

This is a handy option if you have children who are too young to handle money themselves, or if you don’t trust a beneficiary to spend it as you would wish.

For example, if you’d like to leave everything to your brother – but he’s addicted to gambling – you could appoint a trustee to ensure he’s only given certain amounts of money for specific purposes.

By leaving a spouse inheritance in the form of a trust, you can avoid paying a certain amount of IHT. When the surviving spouse dies, the funds included in the trust are not classed as part of the estate and are therefore exempt from IHT (although other taxes do apply).

Setting up a trust is should be carried out under the guidance of a trained professional to get the best advice. You can find a local one through STEP (the Society of Trust and Estate Practitioners).

Actually, yes. If you have no family or friends you’d like to give any personal items to, or any children for whom you may need to arrange guardianship, you might still want to give your personal belongings to charities. If you don’t put this in a will they won’t benefit.

Also, if you have family heirlooms or gifts you want to pass on for sentimental value, it’s worth making a will. And if you have any children, it’s really important that you write a will because you will need to say who you would like to look after them if you’re not around.

In the event of the death of the mother – where the mother and father are not married – the father will not necessarily be given guardianship of the children. Social services will place the children with whomever they see fit.

Even if you’re a married couple – as difficult as will planning sounds – you need to plan for the possibility of you both dying at the same time. Who will look after the children then and will there be any money to leave to them?

If your estate is worth less than £5,000 and you have no children, you may well be able to make a will yourself using a ‘write your own will kit’.

If you have assets of over £5,000 – or under £5,000 and have children – it’s a good idea to get a will professionally written.

Solicitors often offer to write their clients a will. This is perfectly acceptable and if you trust your solicitor, it’s a practical way to get your will written.

However, many solicitors actually use professional will writers. They’re generally more qualified to deal with specific issues, particularly inheritance tax planning and trusts.

If you think that your will is likely to be complicated in any way, you should go to a professional will writing company, as mentioned above, which is a member of either The Society of Will Writers or the Institute of Professional Will Writers or STEP (the Society of Trust and Estate Practitioners). In fact, the members of STEP are ones who can help you the most with tax planning. These people are lawyers, tax specialists, and accountants, etc. They specialise in stopping you and your inheritors paying any more tax than you absolutely have to.

Your estate is everything that you own. This includes any property, cars, life insurance, investments and savings, ornaments, jewellery – basically anything with a resale value.

When you die, parts of your estate are sold off to repay any remaining debts. This includes mortgage payments, credit card bills and any other money owed to creditors.

So, if you leave your house to your son – and you still have £100,000 left to pay on the mortgage – your son will inherit the responsibility of either paying the mortgage or selling the house to pay for the mortgage. In this case it’s a good idea to set up a life insurance policy, set in trust. This is specifically to pay off the mortgage when you die. Find out more about life insurance in our article here.

If you die with debts – and your estate is worth nothing – your creditors will remain unpaid and your family will not be responsible for any payment of debts.

A beneficiary is anybody that receives anything from your will. This can even be for something as small as a pair of earrings.

When you write your will, it’s a good idea to appoint executors. These are the people who will carry out all your wishes.

The law only allows four executors to act on one will at any one time.

Executors don’t have to be beneficiaries – but they can be if you like. They can be a friend, family member, work colleague, lawyer – in fact anyone who’s over 18.

If a person dies intestate (without a will) the courts will appoint a person to distribute the estate. It’s usually the deceased’s next-of-kin. They also sort any taxes or funeral costs, and are termed an ‘administrator’.

In 2007, the term lasting power of attorney (LPA) replaced the term enduring power of attorney (EPA).

An LPA is the document (instrument) under which you (the donor) appoint a person or persons (your ‘Attorneys’) to manage your affairs should you become physically or mentally unable to do so for yourself.

You appoint people you trust to be your attorneys in the event that you can no longer look after yourself. They are in charge of your property, finances, health and welfare.

There are two types of LPA: Health and Welfare, and Property and Affairs. The Property and Affairs LPAs cover everything to do with money – signing cheques, dealing with banks, your property etc. Health and Welfare LPAs allow the attorney to choose a new home for you or to select care options. It also allows them to deal with medical staff as if they were you. However, they do have specific authority to refuse life-sustaining treatment on your behalf, and not everyone chooses to do that.

An LPA fulfills the same role as an EPA used to. But if you’ve made a will using the term EPA it’s probably best to have it updated as it may be invalid.

Probate describes the process a will goes through after the testator dies. The testator is the person who the will relates to.

The executors bring it before the authorities to check that it’s valid and reasonable. They also protect the wishes stipulated in your will.

The Probate Registry grants permission for will execution. A will can fail at probate for a number of reasons, including spelling and grammar mistakes or any misinformation.

If it does fail, the law of intestacy (the condition of no valid will being present) applies.

It depends on the changes that need to be made when getting a will written. Certain will writers give you the option of updating your will for free or for a reduced fee.

If you don’t have this option, you should seek advice as to whether to add a codicil (an extra bit), or whether you need to re-write it completely.

In any case, it’s advisable to review it at least every five years. This ensures it’s up-to-date with current legislation.

It’s vitally important that you keep your will safe and away from any possible water or fire damage. If you decide to keep it at home, we recommend you keep it under lock and key and somewhere you’re not going to forget where it is!

It’s also important that you’re not the only person that knows where it is. If you are, and you die, it won’t necessarily be found and the whole process will have been for nothing.

Most will writers offer a storage facility for a small fee. Providing they don’t charge an extortionate amount for this service, we advise you take them up on it when getting a will written.

Mirror wills are two independent documents that ‘mirror’ each other. But, they do have differences and can be changed or revoked independently of the other. These generally apply to married couples or those in a civil partnership.

A mutual will is pretty much the same. It has an added clause preventing the surviving spouse changing the details of their will when their partner dies.

Many DIY wills fail at probate because of silly things like spelling and grammar mistakes. For this reason, if you have assets over £5,000, or any children – it’s widely recommended you take the professional route.

If you do decide to make a DIY will, buy a will pack from a company you trust. The Post Office offers these, as do WHSmith. They’re only about a fiver and pretty easy to fill in. Have someone proofread and spell check it if you opt for the DIY route.

Your money-making expert. Financial journalist, TV and radio personality.